Hurricane Helene - a blow to price stability hopes?

How the 2024 hurricanes in Florida could change reinsurance pricing and impact insurance markets in 2025

How the 2024 hurricanes in Florida could change reinsurance pricing and impact insurance markets

The recent storm Hurricane Helene, has presented a significant challenge for the U.S. and global insurance markets. This Category 4 storm devastated the southeastern U.S., causing an estimated $20 to $ 34 billion in total damages, although the insurance damages are likely to be smaller. As the insurance industry braces for the financial impact (estimates range from $5m to $15m), Helene's destruction could impact catastrophe risk pricing at the upcoming January 2025 renewals. At the time of this report, Florida is facing a further direct hit from Hurricane Milton which will add to the insurance cost. These storms will impact upcoming reinsurance renewals which could be a lot harder than the market had been expecting a month or so ago.

This article explores the potential ramifications of this recent hurricane on the insurance market, comparing it to past storms and assessing the broader implications for insurers, reinsurers, and policyholders alike.

Testing the insurance market

Hurricane Helene, which struck Florida in late September 2024, is shaping up to provide another critical test for both the US and global insurance markets. With wind speeds reaching up to 140 mph, this Category 4 storm hit the Big Bend region, causing widespread devastation across Florida, Georgia, and other southeastern states. Early estimates suggest an overall cost of between $20 billion and $34 billion range, with $15 billion to$26 billion of property damage. Such is the scale of the losses that Helene’s impact could reshape how insurers and reinsurers approach catastrophe risk pricing, especially in the context of upcoming January renewals.

Less of an impact than Hurricane Ian

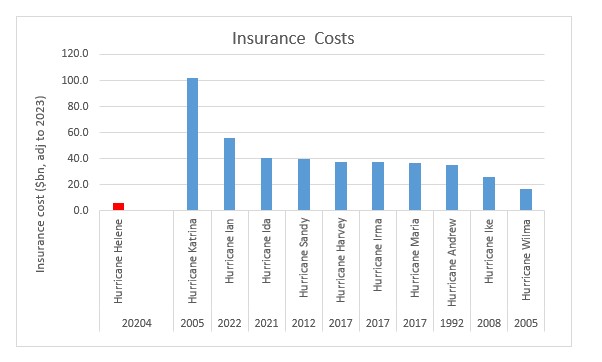

Hurricane Helene’s strength and the sheer breadth of its impact bear striking similarities to Hurricane Ian, which ravaged Florida in 2022. Both storms made landfall as powerful Category 4 hurricanes, but while Ian caused around $65 billion in insured losses, Helene is expected to have a somewhat smaller but still significant financial toll. Helene’s impact on local communities will still be devastating, however. Over 160 deaths have been reported as of early October across six states. Hundreds remain missing and thousands have been displaced.

Figure 1: Comparison of hurricane costs in the USA,adj for inflation3. Source: Aon

Particularly hard-hit are homeowners and small business owners. With property insurance policies across much of the affected region generally not covering flood damage, the National Flood Insurance Program, as the main source of coverage, is expecting a hit.

As Gallagher Re analysis said: “While the wind impacts will be a significant damage driver, there will also be considerable coastal storm surge inundation from the Tampa Bay area northward into the Big Bend. This could result in major losses to the NFIP(National Flood Insurance Program), with the highest active policy take-up rates found in Pinellas, Hillsborough and Pasco counties.”

For many hospitality and retail businesses, the disruption could lead to prolonged closures, worsening the financial outlook for a region already reeling from past hurricanes.

The market's exposure and reaction

Given the size of Helene’s losses, the Market will play a critical role in helping homeowners and businesses begin rebuilding as soon as possible. Speedy payouts will be essential in helping affected regions recover, but the ripple effect on the global market is clear: the much hoped-for stable underwriting, pricing and claims environment is now much more uncertain in January renewals.

Reinsurers will have significant exposure. However, because they have been pushing for higher attachment points on property coverage, AM Best has said that primary insurers underwriting property coverage are likely to absorb most of the losses from Helene. Still, reinsurers may be reluctant to grow their books in such an environment and could look to take ever-higher attachment points as a way to reduce risk. Reinsurance rates could also rise as they did in the 1 July 2023 renewals when Gallagher Re reported U.S. property catastrophe reinsurance rates rose by as much as 50%, with states such as California and Florida increasingly hit by natural catastrophes such as wildfires and hurricanes.

With increased exposure and stress on primary insurers’ books, rates and restrictions may increase for catastrophe-exposed risks. Potentially the whole property insurance market would still be affected, albeit with varying intensity, as well as other insurance lines such as casualty.

What’s next for the London Market?

As Willis reports: “For the second consecutive year, the U.S. experienced an above-average number of tornadoes, hailstorms and straight-line wind events from January to June, resulting in over US $30 billion in insurance claims. Severe flooding impacted multiple areas, including Brazil, East Africa, Dubai, Australia, China, the U.S. and Germany. A Mw7.5 earthquake struck Japan, while Taiwan experienced its strongest quake in 25 years, measuring Mw7.4. Marine heat waves triggered a global coral bleaching event, underscoring the importance of protecting "natural capital” ecosystems. Texas recorded its largest wildfire, burning 426,600 hectares. Meanwhile, severe drought in the Mediterranean exposed the vulnerability of food supply chains to climate risks.”

As the insurance industry braces for what is looking like another record year of catastrophic claims, Hurricane Helene serves as a stark reminder of the increasing risks posed by climate change. Insurers and reinsurers are rethinking their exposure in high-risk regions like Florida, with many expected to push for higher deductibles and more restrictive coverage terms.

While a hardening market will help insurers manage future risks, it may leave consumers with fewer options and higher costs. The future will depend on stronger financial reserves and technological advancements like predictive analytics, flood mapping and advanced pricing tools to better assess risk exposure.

The future of commercial pricing will depend on the industry's ability to leverage technology, including predictive analytics and advanced risk assessment tools, to navigate the escalating risks of climate-related events while maintaining a sustainable and resilient insurance market.

More insights

Significant market changes as reinsurers prepare for the renewal season

After 3 years of market hardening, moderating catastrophe losses and rising reinsurance capital are reshaping renewal dynamics heading into 2026

Data, Speed, and Insight: The Future of Reinsurance Risk Pricing

Harnessing modern analytics and cloud technology to transform actuarial decision-making and strengthen portfolio performance

Autumn Update 2025: Innovation, Renewal, and Market Momentum

Your guide to the latest renewal trends, pricing insights, and standout client success stories